Low-income, independent, hourly, and gig economy workers are particularly hurt by the recession that could be brought on by the coronavirus, which is forcing governments to restrict businesses and limit crowds to stem the number of infections.

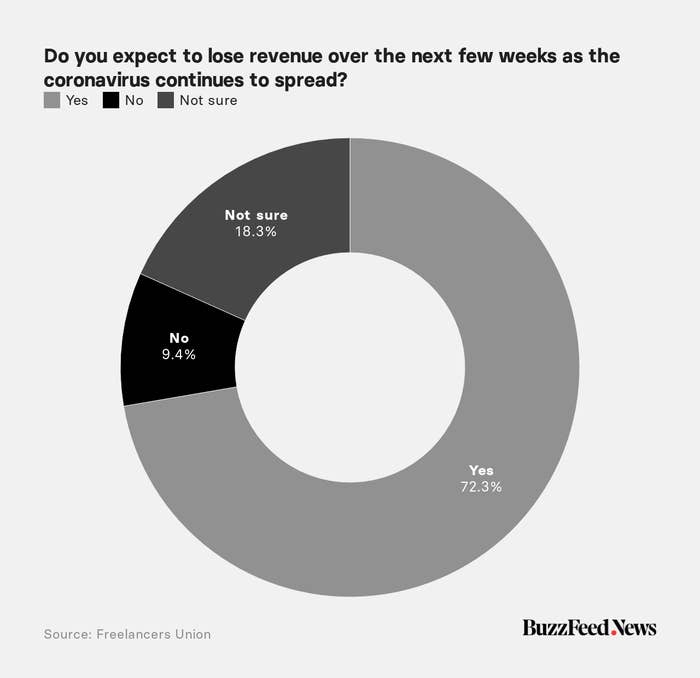

According to a recent survey conducted among roughly 400 members of the Freelancers Union, more than two-thirds of the respondents expect to lose revenue in the coming weeks. Roughly a third of them would be unable to work from home if they had to self-quarantine.

BuzzFeed News spoke to an accountant, a personal finance adviser, and the president of the Freelancers Union to find advice for these workers during the pandemic.

What should I think about first?

If you are on payroll and are laid off or furloughed, you should qualify for some kind of unemployment, Richard Cecchi, a certified public accountant based in Babylon, New York, told BuzzFeed News. Freelancers, independent contractors, and other self-employed people don’t generally qualify for unemployment benefits.

Unemployment benefits are specific to the state and the company you work for, Kimberly Palmer, a personal finance expert at NerdWallet, told BuzzFeed News. It’s important for you to look into what your state may require your employer to pay in case they lay you off, which can easily be done by googling your state and the words “unemployment benefits,” Palmer said.

Then there are decisions that each company makes. Given that these are exceptional circumstances, companies may also decide to provide additional benefits, Palmer said. Uber, for instance, extended paid sick leave up to two weeks for drivers who test positive for COVID-19. Instacart and DoorDash are doing the same for workers who get the virus.

To find out what your company may offer, it could be worth getting in touch with an HR representative.

In terms of health benefits, employees who have been laid off may qualify for continued health care coverage via the Consolidated Omnibus Budget Reconciliation Act (COBRA). As with unemployment benefits, this varies from state to state as well as from company to company.

Last but not least, Cecchi told BuzzFeed News that it’s important to keep an eye out for new bills that local, state, and federal governments might introduce to help employees in response to the pandemic, like after 9/11 and during the 2008 recession.

A bill passed by the House on Sunday, for instance, is supposed to extend paid sick leave to people who work for smaller companies (fewer than 500 employees) or for the government and who tested positive for the virus, are in quarantine, have a sick family member, or are impacted by the school closings.

There’s a lot we still don’t know about the coronavirus outbreak. Our newsletter, Outbreak Today, will do its best to put everything we do know in one place — you can sign up here. Do you have questions you want answered? You can always get in touch. And if you're someone who is seeing the impact of this firsthand, we’d also love to hear from you (you can reach out to us via one of our tip line channels).

What if I can’t pay for rent or other housing on time?

More than 18 million people are currently paying at least half of their income in housing, so missing a paycheck can mean they won’t be able to pay the rent. Palmer suggests talking to your landlord and finding a way to delay payments given the circumstances.

Eviction moratoriums are going into place around the US. Cities like San Jose, California; San Francisco, Seattle, Los Angeles, and Boston have implemented a moratorium on evictions. Kentucky, New York, and Massachusetts are among the states that have halted all eviction proceedings, and advocates are pushing for similar measures nationally, Marketplace has reported. This situation is changing day by day, so it’s important to keep an eye out for any announcements from your local government.

Tenant right laws vary from state to state, and the Administration for Children and Families has a helpful rundown of some basic information on your rights in each state (its guide is geared toward refugees but contains a lot of useful information for just about any tenant).

Thomas J. Waters, a housing policy analyst of the Community Service Society of New York, said that in locations where tenant protections have not kicked in yet, it may be helpful to call your local assembly member or city council member to get a referral to a local tenant rights organization that may help you collect information or evidence that you are acting in good faith, even if you don’t have the income to pay your rent right now.

Are there alternative ways in which I can find income?

“I would really encourage people to see if they are flexible enough to do different work,” Palmer said. “Demand for some things is really dropping but demand for other things is popping up.”

For example, delivery workers are currently in high demand, as restaurants in some states close to sit-in dining but are still open for takeout, and people in lockdown use delivery apps.

Rafael Espinal, president of the Freelancers Union, said a lot of informal organizing is taking place. His union is looking to begin crowdsourcing funds to help people who may face evictions, not have access to health care, or don’t have enough money to go grocery shopping. Espinal and his colleagues will work out criteria to determine who would receive financial support.

“What I’ve been telling independent workers to do is to organize,” Espinal told BuzzFeed, and added that it’s important to make the needs of independent workers known to lawmakers.

“This is the biggest financial crisis that freelancers are facing in modern history and there’s no clear plan as to what they are going to do to help independent workers,” he said.

How much should I continue to save and what are good tips to do that?

Savings are an important factor in weathering economic shocks, especially for people who are self-employed.

“We really encourage people who work in the gig economy to save up 3-6 months worth of expenses for a downturn when work may not come as readily,” Palmer said. “The most important thing in the short term is to look really close look at your budget: what are you spending money on right now.”

This is not something everyone can do, but if there’s even a little bit of wiggle room in your budget, this may help.

Palmer suggested using the “50/30/20” method:

50% to your needs, like rent or food

30% to pay for your wants, like haircuts or dining out

20% to your debt (if you have any) and savings

With this division, people who are hurt by the coronavirus shutdowns should look really closely at your “wants” column and focus on cutting a lot of items in there right away.

If you do have some savings, consider moving them into an online high-yield savings account, she said, where your savings can earn a lot more interest. (You can look up a few here.) If you keep your savings in an account at a traditional bank, you may only earn 0.5% interest. Online accounts could earn you 1.5% or more.

It’s tax season. What should I do if I think I owe money?

Tax bills can be fairly large, depending on how much of your income was not taxed.

If you think that you owe money and may not be able to pay it in one chunk due to coronavirus-related work disruptions, consider filing a 9465-form along with your tax return to apply for an installment plan, Cecchi said. And make sure that you file everything on time.

Treasury Secretary Steven Mnuchin just announced that people who owe less than $1 million can get an extra 90 days after the filing deadline —April 15 — to pay any federal taxes they owe. Lawmakers do, however, recommend to file on time. You should also check in on what your state is doing. The American Institute of CPAs has been keeping track of state-related changes to tax deadlines here.