Nobody likes tax day.

But for the new, amorphous, and ever-growing subset of employees known as gig workers, April 15 can be particularly stressful.

The vast majority of working people in the United States are employees, meaning they file W-2s on tax day. But the independent contractors who deliver groceries for Instacart and drive for Lyft — not to mention those who teach yoga, cut hair, or consult independently — file what are known as 1099 forms, entering them into a whole different, and usually more complicated, tax process.

“It’s quite overwhelming,” says Victoria Esparza of Austin. This is Esparza’s first year as a contractor — she works for a platform called Pretty Instant, as a personal assistant, as well as a nanny and as a merchandiser. To keep track of costs, Esparza writes down her mileage every time she gets in the car. “It’s very complicated,” she says.

People who have made a career out of self-employment know they’re supposed to file quarterly and record expenses, but the thousands of workers who have signed up for on-demand platforms in the last few years often don’t.

Tax professionals know this, of course — and have jumped to educate 1099ers on how to file right.

Matthew Whatley, aka the San Francisco “tax ninja,” realized a couple years ago that most ride-hail drivers in the city “have no idea what they’re doing” when it comes to taxes. “Most of them haven’t filed in multiple years,” he says. “Nobody has a clue. None of them.” Whatley says a driver who’s making $50,000 a year could end up owing $6,000 to $7,000 in taxes, which can be a huge problem if you’re not budgeting for it. Now, Whatley hands out his business cards whenever he gets into an Uber or Lyft.

On the popular driver website UberPeople.net, which has an entire forum dedicated to taxes, Joe Starzyk is just one of multiple accounts that have been reaching out to drivers offering his services as a sharing economy tax professional. Another goes by simply UberTaxPro. Threads are full of questions about deductions, how kids impact taxes, and what to do if you haven’t kept track of work expenditures all year.

“I think the gig economy is great, but people just need to understand there are tax issues — such as quarterly estimates or retirement plan options without a company 401k — that need to be considered,” Starzyk, who has focused on the “underserved” gig economy for a year, wrote in an email. “With the gig economy, so many things get comingled with personal items it becomes difficult to track and record. New Uber drivers often don't realize that they are considered self-employed.”

It’s not just savvy accountants who’ve seen the swelling population of self-employed people in the U.S. as potential customers. Software companies have caught on to the idea, too. UberPeople is full of drivers recommending apps like Hurdlr and SherpaShare for mileage tracking and other financial services.

“When you are a hairdresser, you’re in a hair salon where everyone else is doing the same thing day after day. You’re around other people, so the questions you have, people talk about it,” Randi Sorenson, an independent accountant whose specialty is helping self-employed people, told BuzzFeed News. “Whereas the Uber drivers you have out there are alone.”

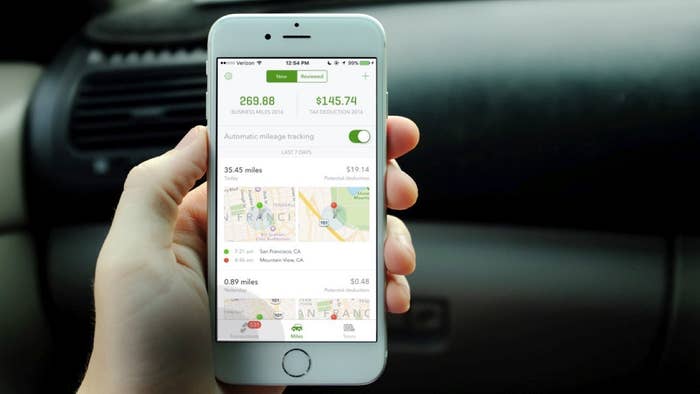

Sorenson is an independent CPA. But she also works with Intuit, an accounting software company that makes a product for independent contractors called QuickBooks Self-Employed. The app keeps track of driver mileage and allows users to swipe left or right for personal or work expenses.

Sorenson says gig-economy workers are at an especially high risk for being caught off guard by how much they owe.

To ensure that Intuit products remain the go-to for all people who need tax help, the company has been marketing its QuickBooks Self-Employed product aggressively via partnerships with on-demand companies including Uber, TaskRabbit, and HourlyNerd. The company even did a Twitter campaign with Lyft in which drivers tweeted about their favorite tax deductions.

My tax deduction were my new tires, I have to make sure I drive my riders with safety! #lyftintuitsweeps https://t.co/YF3n0AnGfl

@lyft @Intuit clearly my favorite deductions are gas and candy! #lyftintuitsweeps

Love that gas & coffee are deductible. Fuel for the car, fuel for the driver. #LyftIntuitSweeps https://t.co/iWOTQgpKcD

Xero, another accounting software company, is trying to cut into Intuit’s lead with a cheaper product for independent contractors called Xero Tax Touch. CEO Jamie Sutherland told BuzzFeed News that 50% of self-employed people surveyed by the company didn’t even know they could file deductions on their taxes. He compared Xero’s solution to Tinder for taxes, saying the goal is to bring a consumer software experience to what is usually a tedious and confusing business.

Despite the obvious-use case, other companies have tread this ground and failed before. Zen99 was a startup that helped 1099 folks with both insurance and taxes, but it shut down in August because of problems with the business model. Benny was a startup — co-founded by an engineer who’s worked at both Uber and Google — aimed at helping people manage all aspects of self-employment. But it, too, recently shut down, according to co-founder Jacob Brody. Others are struggling to make their mark. Bonsai Tax offers “smart tax technology” for contractors. Painless1099 is yet another upstart.

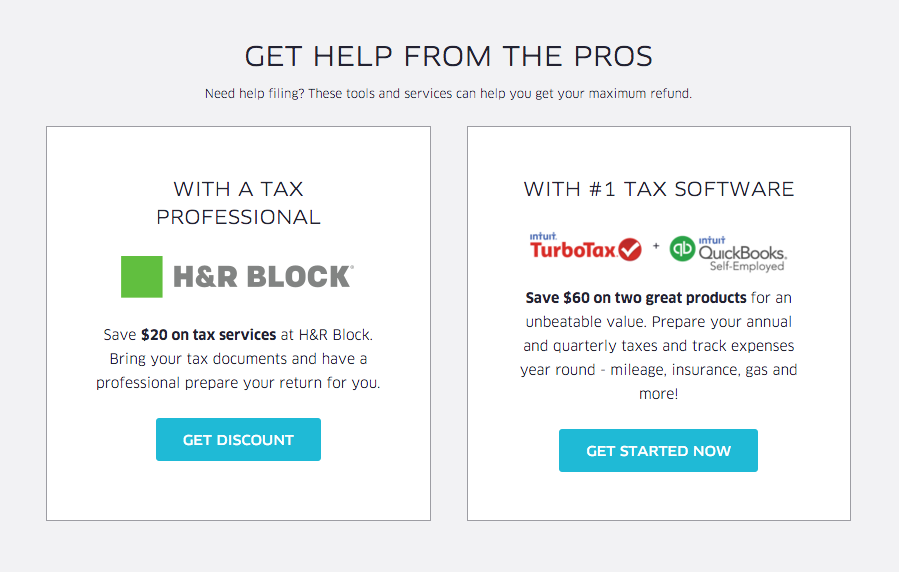

Employers of independent contractors aren't legally allowed to provide tax advice to the workers, because that would imply an employee relationship. This can be frustrating for drivers who feel like the companies they work for are leaving them out to dry. To mediate this, Uber has partnerships with both H&R Block and Intuit through which drivers can get advice, as well as discounted tax services.

There are around 53 million people working as independent contractors in the United States, and that number is only growing — so the number of companies trying to corner that market by building financial tech products from taxes to insurance to banking will only grow, too.

Given how little money those people tend to earn, how hectic their lives are, and how complicated their financial situations are, that’s probably a good thing.