When police showed up at Harry Schmidt's home on the outskirts of Pittsburgh, he thought they were there to help. He was still mourning the disappearance of the beloved forest green Ford F-150 pickup that he’d customized with a gun storage cabinet, and he hoped the cops had solved the crime.

Instead, the officers accused him of faking the theft. The Vietnam veteran was now facing up to seven years in prison.

Schmidt was stunned, but he was even more upset when he found out who had turned him in.

Erie Insurance, one of the nation’s largest auto insurers, had not only provided the cops with evidence against its own loyal customer — it had actively worked with them to try to convict him of insurance fraud.

Erie had even paid part of the salary of the lead detective who knocked on Schmidt’s door that day, as well as that of the prosecutor who went on to charge him with felony insurance fraud. And it would also secretly cover the costs of an expert witness to testify against Schmidt in court.

Schmidt, a grandfather living on disability benefits from his war-related injuries, had no history of theft or fraud. But he found himself the target of an extraordinary alliance between private insurers and public law enforcement agencies — one that transforms routine claims into criminal evidence, premium-paying customers into suspects, and the justice system into a hired gun for a multibillion-dollar industry. It’s an arrangement essentially unheard of in other businesses, and one rife with potential conflicts of interest, as well as grave consequences for law-abiding customers.

“It made me really feel like the law is nothing but another racket," said Schmidt, who said he had to sell many of his possessions to cover his mounting legal bills and stay out of prison.

A BuzzFeed News investigation has found that Erie, State Farm, Farmers, and other giant home and auto insurers around the country have co-opted law enforcement to intimidate and prosecute their own customers — tactics that can help companies boost their profits and avoid paying claims.

Insurance companies provide financial incentives to scores of police departments, prosecutors, and other public agencies to encourage them to focus on insurance fraud, a crime that has traditionally not been a priority for local law enforcement. In some cases, insurance giants even cover the salaries of dedicated prosecutors, detectives, and investigators whose caseloads consist primarily of referrals from those same companies.

The result is that dozens of premium-paying customers across the United States have faced jail for doing nothing more than filing insurance claims for damages to their property.

State Farm and Farmers Insurance both declined to comment on their companies’ fraud-fighting tactics.

“It made me really feel like the law is nothing but another racket."

David Rioux, vice president of special investigations for Erie Insurance, said only a small percentage of claims were flagged as potentially suspicious and that he wasn’t aware of any instances where the company had falsely accused someone of fraud. He declined to comment on specific cases, but said the company follows laws requiring it to report fraud to law enforcement and it’s up to those agencies to decide whether to bring criminal charges.

BuzzFeed News examined 27 cases around the country in which people were falsely charged with felonies based in whole or in part on evidence insurers provided to law enforcement. In Indiana, State Farm helped detectives craft an arrest warrant for a contractor who was charged with 14 felonies. All charges were ultimately dropped when the evidence turned out to be deeply misleading — but not before the insurance giant’s allegations had destroyed his business. In Georgia, a local prosecutor relied on lab tests provided by an insurer to charge a woman with arson, resulting in a three-year ordeal in which she ended up homeless, only to drop the charges when the test results proved unreliable. And in Wisconsin, a man spent nearly three years in prison based on now-discredited science used by an insurance investigator until his conviction was overturned.

In these and other instances, law enforcement agencies have outsourced the hard work and substantial expense of building insurance fraud cases to the industry itself — relying heavily on evidence produced by insurers to prosecute their customers. But those insurers have a strong financial stake in the outcome: Criminal charges help bolster a company’s decision not to pay a claim, and serve as a powerful disincentive for others to file claims of their own.

Got a tip? You can email tips@buzzfeed.com.To learn how to reach us securely, go to tips.buzzfeed.com.

That has led to a culture inside some insurance companies where customers are viewed with suspicion and investigators have been observed openly celebrating when they manage to get them arrested, according to interviews with former employees. In an email reviewed by BuzzFeed News, for example, one of State Farm’s star fraud investigators celebrated one such arrest by circulating a stick figure drawing depicting the man — who it later turned out had been wrongly accused — being raped in prison.

It’s impossible to say how often innocent customers are the victims of false charges, because much of the potential evidence is hidden from public view by the companies themselves. In one case, investigators at State Farm withheld several crucial reports contradicting their fraud allegations from the bundle of evidence they handed over the law enforcement. In another, a Farmers manager admitted under oath that there was an “unwritten policy” within the company to withhold evidence from customers that could help prove their innocence.

Policyholders, meanwhile, often find it difficult and expensive to fight back, leading many to walk away from claims or face pressure to take plea deals for crimes they didn’t commit. And even those individuals who are able to successfully bring lawsuits against insurers are usually obliged to sign confidentiality provisions as part of the terms of any settlement, making it difficult if not impossible for others to find out what happened.

But by reviewing hundreds of court records from around the country, complaints filed with state regulators, and internal company records, and interviewing dozens of former insurance company employees, BuzzFeed News uncovered a system that has ensnared countless innocent people.

In Florida alone, state law enforcement received roughly 14,500 suspected fraud referrals about homeowners and vehicle claims in the past five years — the vast majority of them from insurance companies. Yet authorities determined that in more than 75% of the cases, there was not enough evidence to move forward with a criminal investigation. And regardless of whether fraud accusations turn out to be false, many sit in databases shared among insurers, where they can haunt people if they ever have to file another insurance claim.

These tactics can be applied with impunity, thanks to legislation in all 50 states restricting the ability of customers to sue insurers for wrongly accusing them of fraud — unless the customers can prove the allegations were malicious or made in bad faith.

The legislation was crafted with help from insurers, which worked to get versions of it passed across the country.

“The whole system got corrupted.”

But critics say that the way the law has been implemented favors insurance companies’ commercial interests while failing to provide adequate protections for innocent people.

“The whole system got corrupted,” said Tim Ryles, former Georgia insurance commissioner and chair of the National Association of Insurance Commissioners Antifraud Committee, who helped pass a version of the legislation.

Insurance fraud is a real problem. Entire organized crime rings are dedicated to staging accidents in order to collect insurance money, for example, and industry groups say phony claims cost insurers billions of dollars a year, much of which is passed along to customers in increased premiums.

Insurers say that funding police and prosecutors, and referring criminal cases to them, is critical to efforts to root out fraud, since many law enforcement agencies lack the resources or expertise to bring complicated cases.

These efforts to fight phony claims have netted insurers at least a sevenfold return on investment since the ’90s, according to the Coalition Against Insurance Fraud, a nonprofit that receives most of its funding from insurance companies.

That yields a real benefit for policyholders by helping keep rates down, said Dennis Jay, the coalition’s executive director. “Bottom line is that insurers that hurt innocent consumers should be punished severely,” Jay said.

But for people like Schmidt — and other victims of false accusations — the system seems crafted to benefit only the billion-dollar insurance companies and their investors.

Make more work like this possible by becoming a BuzzFeed News member today.

Framed

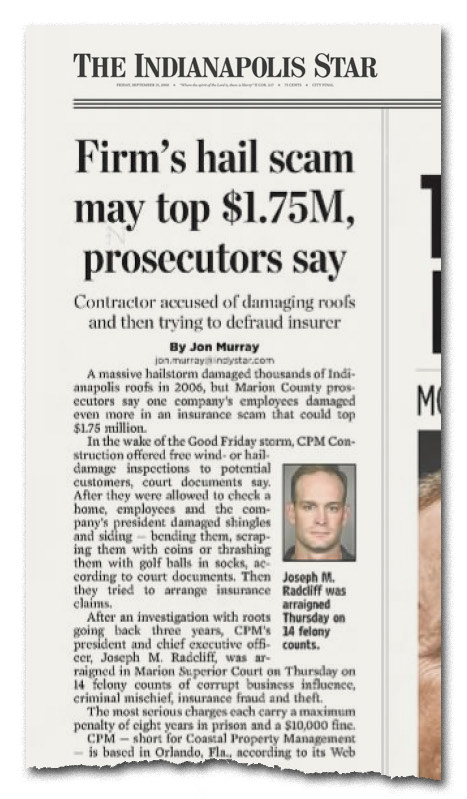

In April 2006, a massive storm damaged hundreds of homes in Indiana, with hailstones the size of baseballs smashing roof shingles, cracking windows, denting cars, and leaving a mountain of costly insurance claims in its wake.

Joe Radcliff, a contractor working in Indiana, started noticing that homeowners with State Farm insurance were having a particularly hard time getting their repairs paid for.

He was hardly the only one crying foul. The Indiana Department of Insurance received 425 complaints from State Farm customers whose claims had been denied following the storm, which generated almost 50,000 claims against State Farm alone.

Radcliff had worked in construction ever since he dropped out of high school to help his family make ends meet. He learned to do everything from cabinetry to roofing to plumbing and eventually launched his own contracting business, which negotiated claims directly with insurers on behalf of homeowners. Over the years, he grew accustomed to arguing with insurance companies about the need for big repairs following major weather events.

But that tension erupted in the fall of 2008, when a group of cops surrounded him on his way to an arbitration hearing related to a disputed claim from the epic hailstorm. The police arrested Radcliff, threw him in jail, and told him he was being charged with 14 felonies, including insurance fraud, corrupt business influence, and criminal mischief.

Although he’d had several run-ins with the law in the past, including a couple misdemeanor convictions, Radcliff had never faced anything like this.

“I'm not going to sit here and say that I'm this angel,” Radcliff said, but these accusations seemed wild. “I'm just a normal everyday guy who was standing up for people.”

When Radcliff’s arrest landed on the front page of the Indianapolis Star, his business took an immediate and massive hit. Suppliers told him they wouldn’t do business with a “criminal,” his referrals dried up, and he was forced to cut his staff from 400 people to just 15.

Eventually, Radcliff learned that State Farm was behind his prosecution. Internal company records show that the insurer began building a fraud case against him in 2007, around the same time it learned he had complained to a local TV reporter that the company had unfairly refused to cover repairs from the prior year’s storm.

“Some of the negative press that has been occurring in Indy has been generated by...questionable contractors in efforts to put pressure on us to simply pay,” an agent in State Farm’s Special Investigations Unit wrote in an email to a media relations executive two days after a segment about the company appeared on the local Call 6 Investigates show. “A good, positive story to indirectly expose some of these practices and help protect consumers would go a long way to helping change the public’s attitudes and perceptions.”

State Farm investigated 10 claims from homeowners who had hired Radcliff. Although other houses in the same neighborhoods also reported extensive hail damage and needed new roofs, investigators determined that some of the ones Radcliff worked on had been intentionally vandalized as part of a fraudulent conspiracy to bilk the insurer.

State Farm tried to pressure at least four of those homeowners into accusing Radcliff of fraud — telling three of them it would pay for the repairs only if they filed police reports alleging that it was the contractor who had damaged the roofs. In another case, State Farm reversed its own determination that a homeowner’s roof was damaged in the storm after it learned Radcliff was involved, locating new experts who now claimed the contractor had vandalized the property.

Some homeowners complained to the Indiana Department of Insurance about the intimidation tactics. One said State Farm even threatened to turn him over to its fraud unit as well unless he accused Radcliff of vandalism.

“It didn’t matter if I was innocent or guilty. They wanted to take myself and my business out.”

Despite the complaints, Tom Cockerill, an investigator for the insurer, took the allegations to the National Insurance Crime Bureau, an industry-funded nonprofit that acts as a liaison between insurers and law enforcement. But Cockerill withheld several crucial reports and customer statements that contradicted the company’s allegations.

The NICB passed the allegations on to the Indianapolis Metropolitan Police Department. Both the NICB and State Farm then worked closely with detectives to build the case, including reviewing the probable cause affidavit leading to Radcliff’s arrest before it was filed in court.

When Radcliff’s case made the local paper and even CNN, Cockerill, the State Farm investigator, celebrated — going so far as to forward a stick figure drawing depicting Radcliff being raped in prison to an NICB investigator. “Enjoy,” wrote Cockerill, who was named “Investigator of the Year” by the International Association of Special Investigation Units for his work on the case. (The association declined to comment. Cockerill, who according to his LinkedIn profile still appears to work in insurance, did not respond to requests for comment.)

But when it was eventually revealed that State Farm had withheld evidence that might have exonerated Radcliff, while key witnesses changed their stories or backed out, prosecutors dropped the charges.

Since then, Radcliff has tried to get several new businesses off the ground, but the accusations still haunt him. “It didn’t matter if I was innocent or guilty,” the contractor said. “They wanted to take myself and my business out.”

A Cozy Relationship

This past April, hundreds of law enforcement agents and insurance company officials gathered in a sprawling hotel in Hershey, Pennsylvania, for the Insurance Fraud Prevention Authority’s annual convention.

The mood was jovial. Enjoying drinks and catered meals, insurance company investigators and police detectives greeted one another as old friends, swapping war stories and trading the latest tips and tricks from the field. Vendors pitched surveillance services and social media monitoring software that allow investigators to covertly track policyholders suspected of fraud. Police officers in business casual attire, mindful of the lucrative investigative jobs open to former law enforcement officers, marveled at how easily insurers were able to obtain the kind of private information that law enforcement can get only with a court order — bank and phone records, for example — thanks to policy contracts that require customers to cooperate with investigations.

Versions of this fraud conference occur across the country. But nowhere is the relationship cozier than in Pennsylvania, where the state Insurance Fraud Prevention Authority not only organizes the annual meeting, but pays the salaries of dozens of police officers and prosecutors.

The IFPA was created by the state legislature in 1995, in response to lobbying from insurance companies that said rampant fraud needed to be dealt with more aggressively. By law, every insurance company operating in the state is required to contribute a percentage based on the premiums they collect from customers.

Insurance company officials make up the majority of the authority’s board, which last year doled out $14 million in targeted grants to fund the work of roughly 100 prosecutors, investigators, and support staffers across the state dedicated exclusively to rooting out insurance fraud.

Those law enforcement officials collected $5.6 million in restitution from people accused of insurance fraud in 2018, money that went back to the insurance companies. According to the IFPA’s annual report, the most commonly investigated cases don’t involve sophisticated organized crime rings, but individual policyholders ages 18 to 34 with no prior criminal record.

It’s an unusual arrangement that doesn’t exist in other states, though law enforcement agencies in several others, including California, Massachusetts, and Nevada, do collect money from insurers to fund fraud investigations.

The offices of the Philadelphia district attorney and the Pennsylvania attorney general are guaranteed a portion of the money each year. But other law enforcement agencies in the state must apply to receive continued funding. If the board members feel that the agencies are not conducting enough investigations or making enough arrests, it can terminate funding.

Although that’s rare, funding for the Montgomery County district attorney, just outside Philadelphia, was recently cut off. The IFPA was displeased the office's arrests and prosecution numbers, its executive director, Tom Donahue, said in an interview, and the district attorney’s office didn’t bother to reapply for the money. (A spokesperson for the district attorney’s office said its arrests were low because state investigators were handling these types of cases in their region.)

Donahue, who previously worked as an investigator for several insurers, said the funding model doesn’t pose a conflict of interest. “The referrals are reviewed by seasoned professional prosecutors who accept or deny referrals based on the evidence provided,” he said. “I have not seen any evidence of criminal charges bolstering a company’s decision not to pay a claim or serve as a disincentive for legitimate claims to be filed.”

Roaming the halls of the IFPA's annual convention at the Hershey Lodge, Patrick Gleason, a detective who specializes in insurance fraud at the Philadelphia district attorney’s office, was one of the few voices of concern over the relationship between law enforcement and the insurance industry. He said his office works hard to ensure investigations are conducted independently, but avoiding undue influence from the insurance companies requires vigilance. Over the years, Gleason said he’s witnessed one insurer withhold exculpatory evidence in a felony case, and taken calls from insurance officials asking for secret information he legally cannot give out.

Appearing on one of the convention’s panels — titled “Arson for Profit” — he warned insurers about the dangers of collaborating so closely with the cops. “You can’t work with us,” Gleason implored. “It will get you in trouble and it will get us in trouble too.”

Pressure to Take a Deal

When the Allegheny County district attorney’s office in Pittsburgh received its first industry-funded grant for a prosecutor dedicated to insurance fraud in 1998, Nicholas Radoycis Jr. was an obvious candidate to lead the unit. He’d worked briefly as an insurance underwriter, been a volunteer firefighter for over a decade, and had already worked closely with insurance company investigators while prosecuting several arson cases before the unit existed.

Radocyis, short with a full head of white hair and round, thin-rimmed glasses, went on to handle nearly every insurance fraud case in the county for the next two decades until his retirement this past spring.

His salary of $93,549, as well as those of the police officers assigned to work on insurance fraud, was entirely covered by grants from the Pennsylvania Insurance Fraud Prevention Authority. Last year, the money that the insurance board gave Allegheny County to go after insurance fraud came to $728,202, all told, and over the past decade his office handled more such cases than almost any other agency in the state.

Insurance fraud charges filed by the Allegheny District Attorney’s office almost never made it all the way to trial — fewer than 3%, according to public records — and as a result the evidence he relied on to bring criminal charges was rarely scrutinized.

Instead, he acted less as a public prosecutor than as a debt collector for the insurance industry. Many of his cases were resolved in private negotiation with the defense, then approved by a lower-level judge, known as a magistrate judge, in a cramped basement courtroom below a banquet hall and a nail salon. Defendants were generally let off with no admission of guilt if they agreed to pay a fine, complete community service, and reimburse their insurers for the money they had claimed.

When Radoycis brought fraud charges against Michael Hart in 2017, there was every reason to assume he’d take a deal as well.

Hart, a 59-year-old bus driver, had been rear-ended on the way to work more than a year earlier, an accident that no one held to be his fault. But the other driver’s auto insurer, Progressive, took issue with his claim that his wrist had been seriously injured in the crash. Following the accident, the other driver had assaulted Hart, according to a police report. A Progressive investigator provided evidence to Radoycis’s fraud team suggesting Hart had been injured in that altercation instead of the crash, which would mean the company was not responsible for paying the claim. (Progressive acknowledged that it provided information about Hart in response to a request from the police, but said it did not suspect him of fraud.)

As the case moved toward trial, Radoycis offered Hart the same deal he’d offered so many times before: He would be put on probation for a few months, but could walk away without admitting guilt and ultimately get his record expunged.

Reviewing the evidence, Hart’s defense lawyer, Joe Otte, was surprised by how little independent investigation the detective, Richard Nowakowski, seemed to have done beyond the file that had been handed to him by Progressive. “It looked like he flipped through it, signed off on it, and it went to prosecution,” he said. Nowakowski, who has since retired, did not respond to requests for comment.

“I don’t understand how people can sleep at night when they ruin innocent people’s lives.”

Still, Otte cautioned his client about the risks of fighting the charges. On a bus driver’s salary, Hart simply couldn’t afford the $7,000 or more that expert witnesses would charge to testify in his defense — and without that evidence, he’d have a harder time proving his innocence. If he lost at trial, Hart could be looking at up to seven years in prison.

“I was very concerned that he was not understanding the ramifications” of fighting this case, said Otte.

But Hart was confident. He had no criminal record and figured if he wasn’t a liar, the law would be on his side. He stubbornly refused to take the deal, and started working more overtime to cover his mounting legal bills.

Finally, this past fall, he had his day in court. To Hart’s immense relief, the judge found that Radoycis hadn’t met the burden of proof required to convict Hart of insurance fraud, and found him not guilty.

The Allegheny County district attorney’s office said its efforts to fight insurance fraud are fair and effective. The industry-funded operation “not only helps to hold people who abuse the system accountable, but also serves as a deterrent to others contemplating similar behavior,” a spokesperson said.

But Hart soon found that criminal accusations can continue to haunt people even when they’re acquitted. Unexpunged charges can show up in background checks, making it harder to get a job or rent a home.

Despite the courtroom victory, his own insurer, Liberty Mutual, dropped his coverage. He said he’s been unable to convince Pennsylvania’s insurance regulator or other authorities to investigate what happened to him. Liberty Mutual declined to comment on the matter.

“I don’t understand how people can sleep at night when they ruin innocent people’s lives,” Hart said.

A Critical Change

Even those who manage to prove their innocence have little recourse — thanks to a law that was written with the help of insurance companies.

In 1992, an industry study estimated that 1 in 10 claims paid by insurers were fraudulent. Many in the business find that statistic to be unreliable. But the study, which continues to be widely cited to this day, spotlighted what soon came to be viewed as a tremendous business opportunity: Companies realized they could save millions by aggressively denying claims they deemed fraudulent.

Three years later, the Coalition Against Insurance Fraud, a group composed of insurance companies, consumer groups, and other stakeholders, helped craft model legislation that guaranteed companies broad immunity from any customer who wished to sue for being wrongly accused of fraud. In exchange, companies are required to report suspected fraud to law enforcement. The coalition then went to work getting versions of that legislation passed across the country with help from state insurance regulators.

“They’re saying, ‘We have a right to be wrong, and if we’re wrong you can’t sue us.’”

Granted that kind of immunity, insurers felt far more willing to accuse their own customers of crimes. “Overnight, we just saw insurers gladly report fraud,” said Jay, the executive director of the coalition.

But that’s left consumers at an unfair disadvantage, critics say.

To successfully sue over false fraud accusations, a consumer has to prove the insurer acted with malice or bad faith — a high bar that typically requires expensive litigation to obtain internal company records.

“They’re saying, ‘We have a right to be wrong, and if we’re wrong you can’t sue us,’” said Amy Bach, the executive director of United Policyholders, a consumer group that advocates for insurance policyholders. “You know how you have fishing nets for tuna and it also catches dolphins in the same net? If the system is too aggressively or too broadly applied, it hurts people who did not commit fraud but can’t muster the resources to defend themselves against the juggernaut of a big corporation.”

Today, the industry relies heavily on guidelines from the National Insurance Crime Bureau to help determine which claims should be scrutinized for fraud, a process that can involve extensive delays while people are without a home or car.

A nonprofit funded by more than a thousand insurance companies, the NICB was founded in the early 1990s. NICB agents help vet thousands of suspected fraud reports shared by insurance companies, embed in task forces with the FBI, and help craft threatening letters to customers suspected of fraud on behalf of state insurance regulators.

"Ninety-five percent of the time there is not a problem … But the other 5% catches a lot of innocent people.”

They also help develop “red flag” indicators to help companies spot fraudulent claims. Consumer advocates say some of these red flags — such as “insured is unusually knowledgeable regarding insurance” — seem overly broad. Others, they say, could disproportionately target low-income people, such as “experiencing financial difficulties.”

“The idea that if you have financial difficulties you’re inclined to defraud others is deeply troubling to me,” said Doug Heller, an insurance expert for Consumer Federation of America.

The NICB, for its part, said that no single indicator is proof of fraud; instead, the indicators serve merely as suggestions to help insurers identify which claims deserve greater scrutiny.

But Karl Smith, who until last year handled fraud cases as part of his job as a lawyer for Farmers Insurance in Nevada, said that based on his experience, that industry’s methodology still makes for a whole lot of false positives. "Ninety-five percent of the time there is not a problem. The claim is paid,” Smith said. “But the other 5% catches a lot of innocent people.”

Outsourcing Investigations

Shanna Shackelford was a 21-year-old nurse’s aide and part-time employee at Walmart living in Carrollton, Georgia, when the house she was renting burned down. At least she’d bought renters insurance from State Farm, she thought as she watched almost everything she owned go up in flames.

At first, State Farm put Shackelford up at a nearby hotel, but two months later the insurer’s fraud investigators concluded she had intentionally set the fire, denied her claim, and referred her case to local law enforcement.

Three days after Christmas 2009, they stopped covering her temporary housing and Shackelford, unable to pay the rent herself, was kicked out of the hotel with nowhere to go. A few months later she was charged with criminal arson, which carries a sentence of up to 20 years.

State Farm and the landlord’s insurance company had collected samples from the scene of the fire, testing them for gasoline or other accelerants that might suggest the blaze was set intentionally. Eager to keep costs low, the Carrollton Fire Department, which helps local police with fire investigations, relied entirely on the reports given to it by the insurers rather than doing any of its own testing.

In a letter begging a pro bono attorney to take on her case, Shackelford wrote that she had “lost countless jobs, lost my home, my dogs, and had to sell everything I own to make it to this point. I now sleep in my car, and occasionally family members will allow me to come over to shower.” She was no arsonist, she protested: “I just don't wanna die without someone knowing what these people are doing to me, and how I have cried, pleaded, and begged for help.”

The lawyer took her case and soon tracked down a fire expert who raised concerns about the reports that State Farm had handed the police. The evidence, the expert concluded, in fact strongly suggested the fire had been accidental and that Shackelford wasn’t responsible.

More than a year after the fire, the only remaining physical evidence were the samples the insurers originally sent to the lab. The prosecutor acknowledged that “the State’s case was based primarily on the insurance company’s analysis as to the cause of the fire.” Since it had proved impossible to obtain the insurers’ samples to retest, the charges were dropped.

It took years for Shackelford to get the charges expunged, during which time she said her status as a suspected felon made it extremely difficult to rent a new home or find a job. She’s now starting to get back on her feet and plans to get a law degree.

The Carrollton Police Department is hardly the only law enforcement agency to rely heavily, if not entirely, on evidence produced by insurers in fraud cases.

In Phoenix, the county attorney’s office dismissed felony charges against a woman facing 27 years in prison after the prosecutor determined Farmers Insurance and the local fire department investigator had an “incestuous relationship” and had ignored evidence that pointed to the policyholder’s innocence.

In Wisconsin, Joseph Awe spent nearly three years in prison because a local fire investigator recommended charges based on the determination by Mt. Morris Mutual Insurance that he’d burned his bar down to collect insurance money. That assessment turned out to be based on bad science, and Awe was released from prison in 2013.

Got a tip? You can email tips@buzzfeed.com.To learn how to reach us securely, go to tips.buzzfeed.com.

And in a 2010 criminal case in Pennsylvania, a judge became so frustrated with the testimony of an expert who seemed biased in favor of the insurance company that he threatened to refer him for prosecution for perjury.

The expert, hired by Erie Insurance, had opined that a faulty hair dryer could not have caused the fire that destroyed a policyholder’s home. But when the defense uncovered information suggesting it could have been the appliance after all, the expert went out of his way to side with the prosecution.

Experts “are supposed to be independent, notwithstanding the fact that they’re hired by one side or the other,” the judge said, according to the trial transcript. He admonished the prosecutor who was relying heavily on the expert’s testimony to make his case: “I want you to take your witness aside and tell him that no matter what the jury does, if I conclude, based on testimony, that he has not told the truth, I will advise the district attorney’s office to file perjury charges against him.”

Shortly afterward, the prosecutor dropped the charges. The expert, Richard Wunderley, and his employer, EFI Global, declined to comment.

A spokesperson for Erie Insurance said the company would “never knowingly work with an expert with a known bias or accused of perjury.”

Wunderley continues to provide expert testimony in insurance cases, and was recently named president of the Pennsylvania chapter of the International Association of Arson Investigators.

Even When You Win, You Lose

In late 2010, Harry Schmidt’s case finally went to trial.

To cover the thousands of dollars in legal fees he was racking up to defend himself from charges he had plotted to steal his own truck for the insurance money, he had begun selling parts of his antique gun collection.

Over four days of testimony, Schmidt’s lawyers poked several holes in the prosecution’s fraud theory. The district attorney’s office argued that Schmidt must have been involved in the vehicle’s disappearance because the truck could only have been taken with one of the two factory-issued keys, both of which were in his possession. On the stand, the expert who had written the report that Erie Insurance gave to the police ultimately conceded that he couldn’t rule out other ways the car could have been stolen without a key, such as using a tow truck. And the prosecution offered no explanation for how Schmidt, who was in Florida at the time his truck disappeared, could have been involved.

In the face of such doubts, the judge found Schmidt not guilty.

But his fight with the insurance industry was far from over.

Schmidt, by then 59 and nearly broke, filed a lawsuit against Erie in hopes of recovering some of his legal expenses. Although Erie argued that it was immune from civil liability for reporting fraud, Schmidt’s lawyers contended that they had grounds to sue because the insurer had acted maliciously, failing to properly investigate the facts before passing his file on to prosecutors.

Erie responded by going on the offensive: It countersued Schmidt for fraud, even though a judge had just found him not guilty. The insurer — which had originally paid the veteran’s $28,101 claim for the stolen truck, only to help him get criminally charged soon thereafter — now wanted to recoup the money it had paid out.

“For State Farm, that’s nothing. If you or I did that, we’d be in prison.”

The competing lawsuits provided Schmidt access to internal company documents, which soon revealed Erie’s deep entanglement in the prosecution’s case. Although the expert that Nicholas Radoycis, Allegheny County’s specialized insurance fraud prosecutor, relied upon had claimed under oath, “I don’t receive any compensation for my testimony,” invoices and checks proved he had in fact been paid by Erie for his three appearances.

Soon after Schmidt presented that evidence, Erie settled with him for a confidential sum without admitting any wrongdoing.

Like Erie, State Farm also doubled down on the contractor Joe Radcliff when he was arrested, suing him for fraud while his criminal case was still pending.

Radcliff fought back, countersuing the insurer for defamation after the criminal charges against him had been dropped.

The civil court eventually determined that the insurer had investigated Radcliff not because of a good-faith effort to root out fraud, but because it was unhappy with his work helping State Farm customers file expensive claims that it didn’t want to pay. State Farm had used “deception, misinformation, intimidation, and omissions to ultimately present an investigation report that was fraudulent,” the judges concluded.

In 2014, Radcliff received a $14.5 million verdict — one of the largest defamation verdicts in US history. Much of it went to covering his legal bills and loans he’d taken out to survive during the years the lawsuit was pending.

He says it’s hard to think of the money as much of a victory.

“For State Farm, that’s nothing,” Radcliff said. “If you or I did that, we’d be in prison.” ●

Opening illustration by John J. Custer for BuzzFeed News.